As a CFO, one of the common reasons I am brought into a manufacturing organization is to solve the mystery of “Why our sales are growing, but profits low?” Most of the companies I work with have rigorous quoting processes that they assume will protect them financially, but in the end their actual monthly profit margins often fall short of quoted (and anticipated) profit margins.

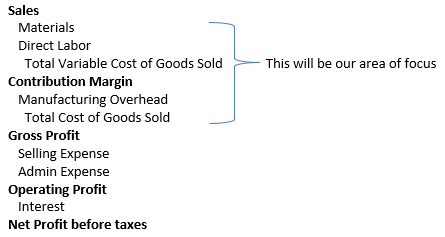

Before diving into an examination why profit margins lag behind sales growth projections it is important to take a look at accompanying financial reports. These are categories from a simplified manufacturing income statement:

In this article we will discuss materials, direct labor and manufacturing overhead as they relate to gross profit.

Some companies have quoting systems that calculate to the gross profit level including a target number that covers selling, general, and administrative (SG&A) expenses. Other companies add SG&A into their quoting process to give them a target operating profit. Whether including or not including SG&A expenses directly, the profit margins will still be accurate if the factors that represent these expenses are accounted for accurately.

Let’s look at the components of production costs as related to the quoting process to determine where an organization can go astray.

Bill of Materials

Creating a detailed bill of materials is the core of any quoting process or cost-setting standard.

I seldom find a problem with the material quotes and standards except for instances where material costs change between when the quote was generated and when the contract was signed. In scenarios where significant change has occurred, a new quote should be generated to reflect increased material costs accurately.

Another area for review with materials is the scrap rate assumption. When scrap rates are exceeded, and proper reporting is not in place to capture the extent of the loss, materials costs can increase substantially.

Direct Labor & Overhead

Typically, profit margin shortcomings are due to issues with direct labor and overhead rates.

Organizations that have not updated their quote (or standard) rates for labor and overhead in the last year, hamper profit margins by using outdated numbers to acquire new business. Given the frequent changes in labor rates and benefits, as well as the impact of growth, rates can change significantly from year to year. Therefore, an annual review is essential for manufacturing companies of all sizes.

Monthly financial reporting should track labor and overhead rates to determine trends and establish an appropriate window for revising them.

Even amongst companies that update their rates regularly, there can still be calculation omissions that reduce the quoted rates below their actual values. The result is a discrepancy in profit margins that can sink even the fastest growing manufacturers.

Direct Labor Rates

Any employee involved in the production routings is part of the direct labor pool. Direct labor rates can either be calculated by work center or combined as one overall figure. Typically, if there is a substantial difference in pay rates between work centers, they will be broken out to allow for better financial analysis. However, if workers tend to move between work centers frequently, calculating rates for individual work centers can be complicated, resulting in the use of one overall figure.

Rate Calculation

Once the direct labor pool has been identified, you can calculate the direct labor rate.

Some organizations use the average pay rate of the work center or the pool (ex. $20/hr.) and forget to include other costs like benefits and employer taxes. Things like medical benefits, accidental death and dismemberment insurance (AD&D), and workers’ compensation taxes (L&I) can add 20-30% to the pay rate depending on employer selections. These additions can easily bump up that $20/hr. pay rate example to $25/hr.

Non-Worked Time

While quotes are usually calculated based on hours worked on a machine, workers cost an organization money even when they are not working. Non-worked hours can include vacation, company holidays, and lunch breaks. So, if an average employee receives 10 days of vacation, 9 holidays per year, and breaks that are not included in the routing times, add 0.5 hours per day for 240 days, that results in 167 hours not worked. That is approximately 8% of 2080 paid hours annually. Suddenly the $25/hr. rate becomes $27/hr. when the additional 8% for non-worked time is included.

Non-Production Time

While on the job, workers spend time doing things other than producing product. Non-production time occurs when workers carry out functions like materials handling, taking inventory, data input, attending meetings, and engaging in re-work. Furthermore, machine downtime results in non-production time as well. Non-production time can have a huge impact on direct labor costs, which means that it should be closely tracked to give better insight into where an organization can improve. In some manufacturing operations, this can be as much as 10% of a worker’s day. This 10% addition brings the $27/hr. rate to $29.80/hr., which can result in a noticeable difference in profit margins.

Labor Efficiencies

The direct labor rate calculation above assumes a labor efficiency of 100%. However, perfect efficiency is unrealistic, which is why all inefficiencies should be reported and analyzed. Systems need to be implemented to track these inefficiencies and a determination needs to be made as to whether they are inherent to the process (and thus should be added to the labor rate) or are solvable (and therefore should not be passed on to the customer). Obviously, this can affect profit margins as well, leading to variances. For instance, if efficiency is only at 80-90%, labor cost can increase by another $3-6/hr.

Unfortunately, many systems do not handle labor efficiency reporting very well. To get a true understanding of inefficiencies, there must be a procedure in place to capture floor data related to actual work performed that is broken out by product, process, job, etc. (Whether it is reported daily, weekly, or monthly depends on the sophistication of the data capture procedures and the production or ERP system itself.) This data should then be compared to the quoted labor rate to identify any variances. The larger the variance, the more important it is to report, analyze, and respond in a timely manner.

Overhead

After direct labor, it is time to analyze overhead rates. It is helpful to separate out variable overhead from fixed overhead to allow for proper forecasting and budgeting.

Variable Overhead

Variable overhead are costs that fluctuate in relation to changes in production output. These usually consist of things such as manufacturing supplies, utilities, and support personnel. Due to the direct relationship between inputs and outputs in manufacturing, variable costs are rarely the source of profit margin shortcomings.

Fixed Overhead

Fixed overhead, on the other hand, can easily result in profit margin discrepancies, especially in fast growing organizations.

The components of fixed overhead include:

- Indirect Labor – Manufacturing supervisors and managers add to fixed overhead costs, as do other indirect support personnel that are not included in direct labor routing. This may include workers engaged in material handling, maintenance, sanitation, warehouse, planning, expediting, etc. Whether workers are considered direct or indirect, everyone must be included somewhere, otherwise their accompanying costs will not be included either.

- Facility Costs – Rent, repairs, maintenance, property taxes, property insurance, and building depreciation are some common fixed overhead facility costs.

- Equipment Costs – Equipment rental, machine repairs and maintenance, and equipment depreciation are the most common fixed overhead equipment costs.

After the overhead cost pool has been determined, it should be divided by the hours worked (as captured by quoted/standard routings), figuring in both non-worked time and non-production time.

As an example, if your total overhead is $500,000 and you have 10 workers, you would divide $500,000 by 20,800 (2080 paid hours per year for 10 workers) to get an overhead rate of $24.04 per labor hour. If you use the example of 18% of paid time that is not being used for actual production (8% non-worked time + 10% non-production time) then the calculation is $500,000/(2080*82%) for 10 workers. The result is $29.30 per labor hour assuming perfect efficiency. This overhead rate should be factored into your monthly financial reporting to monitor trends. With ever-shifting expenses and production outputs monthly overhead rates will vary, but the overall trend and year-to-date rates can signal the beginning of a deviation from quoted rates before profit margins are severely affected.

Calculation Summary

Note the 34% increase between rates. Once organization-specific production efficiencies are added, this increase can easily approach 50%.

While this may be a worst-case scenario, calculating direct labor and overhead rates is far more complicated than many manufacturers realize. As such, it should be monitored as a part of monthly financial reporting to more closely correlate quoted rates with actual rates.

Next Steps

Calculating direct labor and overhead costs is the first, not the last, step in improving profitability. The most important steps are what comes next. With reliable information, you can make informed business decisions to drive organizational growth. You should focus on questions like:

- How much of your added costs can be passed onto customers without jeopardizing retention?

- How do your actual costs compare to your competitors’ costs?

- Where can efficiency, organization, processes, and product design be improved?

- Where should hiring occur to maximize productivity?

- Should assembly processes be altered to create greater efficiency?

- Where can automation be added?

- Will adding new equipment increase profitability?

- How can product design be altered to make production more efficient?

In larger organizations, cost analysts, certified management accountants, and process engineers will likely tackle these weighty questions, while medium-sized companies will put the burden on their controller or CFO. However, small-sized companies do not have the personnel in-house to handle this level of decision-making. Instead, they need to hire a third-party for support in these areas.

A company like CFO Selections or a freelance manufacturing expert can make recommendations after cleaning up the company’s direct labor and overhead calculations. Smaller manufacturers typically either retain a part-time CFO to ensure they remain on track or are then able to be self-sufficient, because the hired project-oriented CFO or consultant can leave user-friendly templates for less financially savvy in-house employees to use.

About the Author:

Roger Johnson has more than 30 years of private and public company experience as CFO, VP of Finance, Controller, and Director of Finance and Administration. His industry background spans manufacturing, distribution, supply chain, and financial services industries. Roger has over 20 years of extensive international experience in Asia and Pacific Rim countries, and was an expert Foreign Lecturer in the Peoples Republic of China for the Central Institute on Finance.

Roger received his accounting degree from the University of Illinois and an MBA from Pepperdine University. He was previously a CPA.